Market for new trailers for cars and LCVs in Ukraine: analysis of the domestic production segment (Q1 2026)

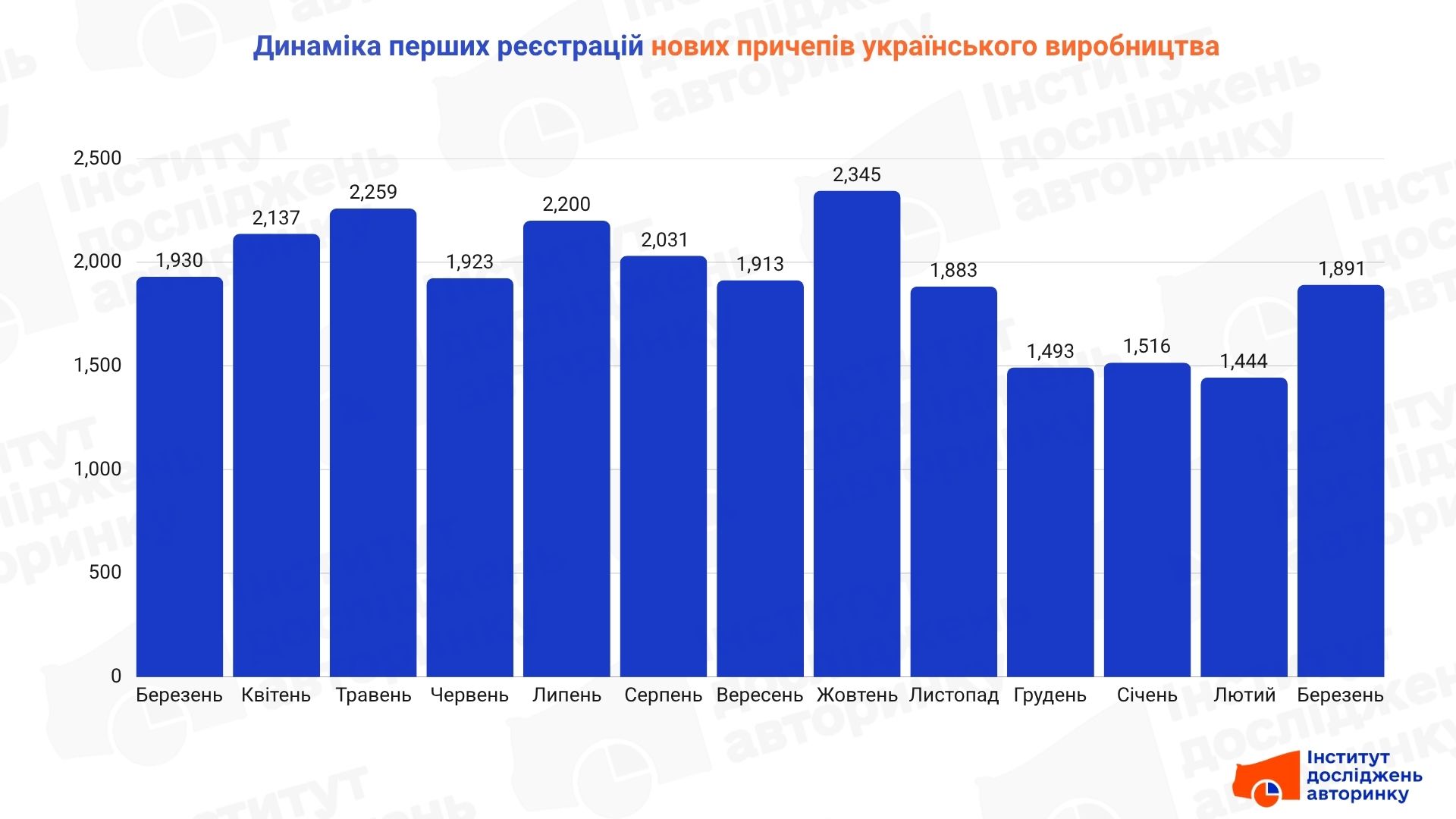

The market for trailers for passenger cars and light commercial vehicles (LCV) in Ukraine demonstrates a pronounced orientation towards the domestic product. In the first quarter of 2026, the segment of new domestically produced trailers became the main driver of the market, providing 4,832 first registrations. For comparison, the volume of imports of new equipment remains minimal ( 35 units ), and the secondary import market ( 132 units ) and domestic resales ( 919 units ) are significantly inferior to the production volumes "from the assembly line".

Market structure by trailer type

There is a clear specialization in the structure of the first registrations of new trailers of Ukrainian production. More than three quarters of the market is occupied by universal solutions for transporting goods.

- On-board — 78.5%

- Platforms — 12.5%

- For boats — 4.4%

- Other types — 4.6%

The dominance of flatbed trailers indicates high demand for auxiliary transport for private households and small businesses amid the rising cost of internal combustion engine-based logistics.

Top 10 manufacturers on the Ukrainian market (Q1 2026)

Analysis of registration data allows us to identify key players that shape the offer in the segment. Most of the capacities are concentrated in the central and northern regions of Ukraine.

- PG (LLC "MP Trailer Plant", Glukhiv) — 1287 pcs.

- Palych (LLC "NVP-Palych", Kyiv) — 980 pcs.

- AMS (Agromotorservice LLC, Starokostyantyniv) — 552 pcs.

- URSA Group (LLC "URSA GROUP", Zaporizhia) — 308

- Dnipro (Cortes-2015 LLC, Kremenchuk) — 297 pcs.

- Pragmatek (PE "Pragmatek", Lutsk) — 245 pcs.

- PAVAM (LLC SPE "PAVAM", Irpin) — 217 pcs.

- TSC (LLC "T-Center Service", Tyvriv town, Vinnytsia region) — 169 pcs.

- Korida-Tech (LLC "Korida-Tech", Vlasivka village, Kirovohrad region) — 162 pcs.

- Kyyashko (Kyyashko LLC, Pavlivka village, Chernihiv region) — 134 pcs.

Results

- Localization as a survival factor. The minimal share of imports (less than 1% in the structure of new registrations) is due to the high cost of logistics of oversized products from abroad. Ukrainian manufacturers successfully compete thanks to well-established supply chains of components (axles, lighting equipment) and lower assembly costs.

- Geographic diversification. Despite the traditional leadership of the Sumy and Kyiv centers, there is activity of manufacturers in Zaporizhia ( URSA group ) and in the west of the country ( Pragmatek, TCS ), which indicates market decentralization.

- Specialization. The platform segment (12.5%) demonstrates stable demand for tow trucks for evacuating and transporting cars, which correlates with activity in the used car import market.

Segment features

The segment of trailers for passenger cars and LCVs is a unique example of sustainable development of domestic engineering in conditions of full market openness. Unlike the car market, the import of trailers (UKT FEA code 8716) is not limited by Euro environmental standards, they are not subject to excise duty, and the import duty from EU countries is 0%.

This segment clearly demonstrates that the Ukrainian auto business can be successful without the "greenhouse conditions" that were once created for the "national manufacturer" by artificially closing imports. A living example of the trailer market, where in the absence of any protectionist barriers, local products account for over 95% of new registrations, proves that true competitiveness is based on product quality and logistics efficiency, not on tax restrictions for competitors.

- Need more information — order it from IDA!