The market for trucks with a gross vehicle weight of over 3.5 tons (excluding tractor units) demonstrated a profound structural transformation in February 2026. Statistics indicate a significant reduction in activity in most segments, reflecting the general business restraint in investing in heavy equipment against the backdrop of a high comparative base last year.

Market volumes and registration dynamics

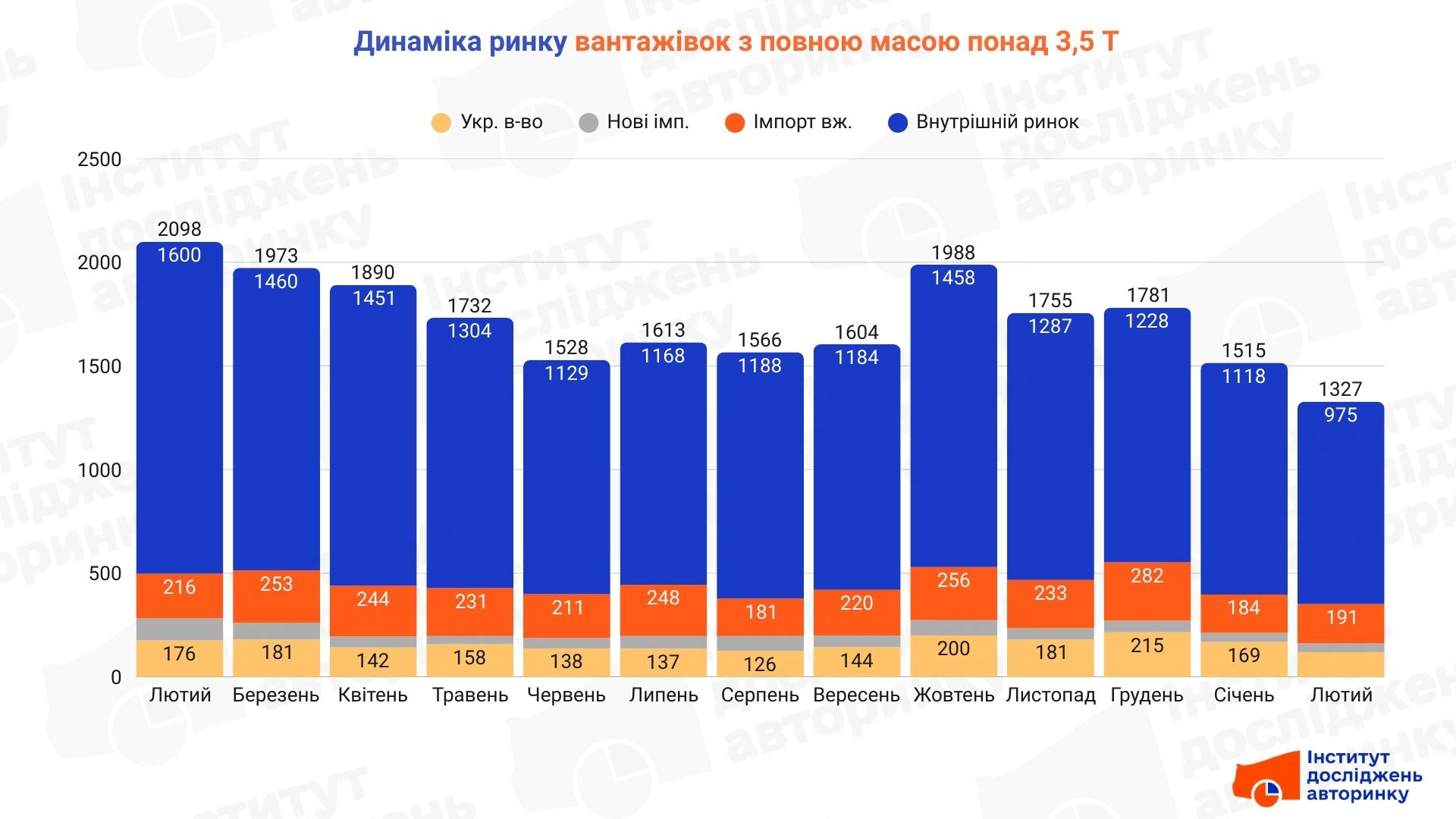

The total number of registrations in the truck segment (single chassis and special equipment) in February amounted to 1,327 units. The main part of the market continues to be formed by domestic resales — 975 transactions. However, this sector shows a steady decline: by 12.8% compared to January and by a significant 39.1% year-on-year (YY).

- Check the history of a car by VIN code before buying at CEBIA!

The most critical decline was recorded in the new truck import segment, where the number of registrations fell by 60.4% compared to February 2025. Domestic production and conversion (new Ukrainian-made cars) also decreased by 32.4% compared to last year, recording 119 units in February. The only segment that showed minimal growth in monthly dynamics ( +3.8% MM) was the import of used equipment, although in annual comparison it also remains in the "minus" by 11.6%.

Internal market: Resource exploitation

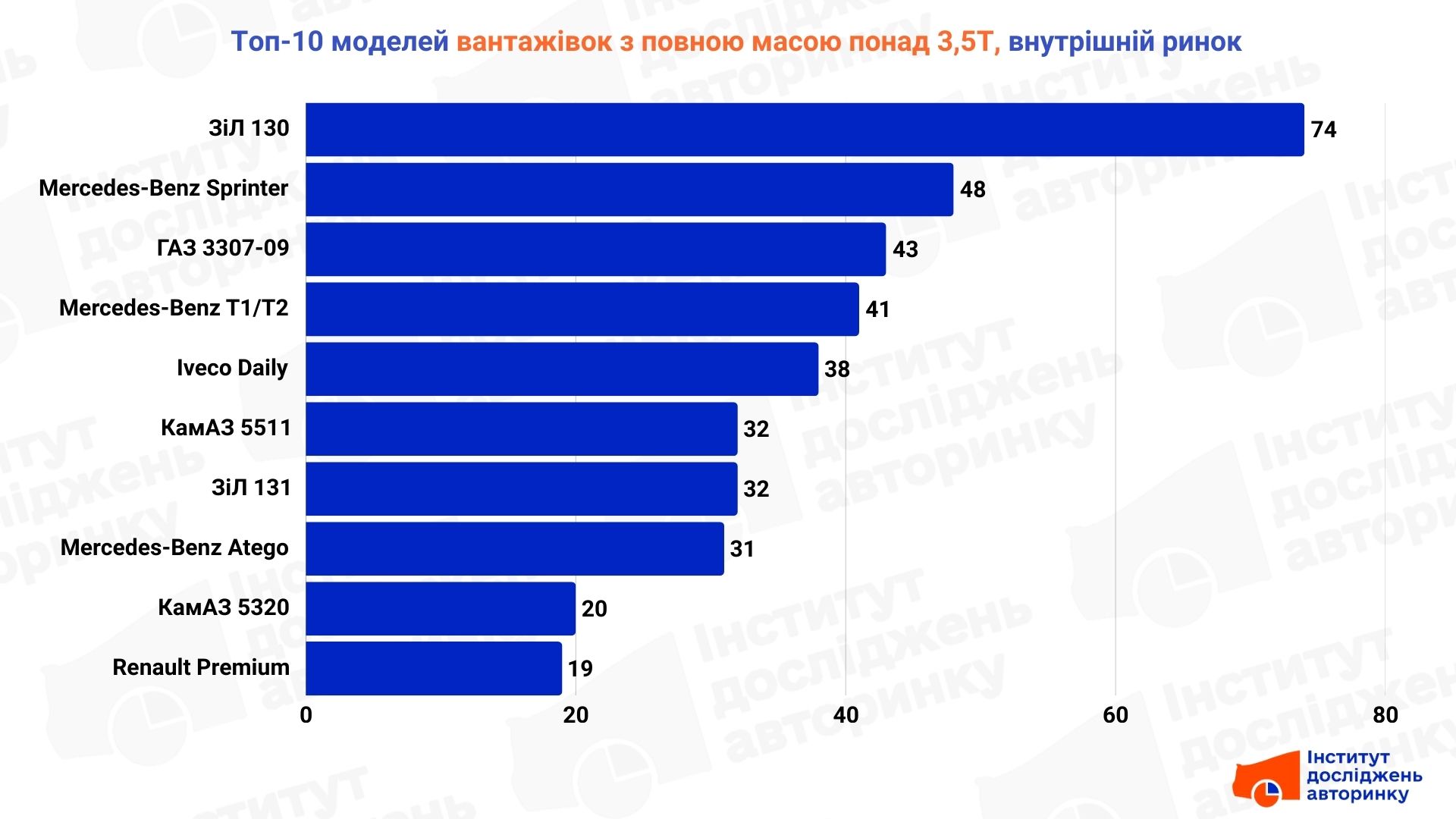

The domestic market is dominated by dump trucks, vans and flatbed trucks. A feature of this segment remains the critically high share of obsolete equipment of Soviet origin, which still forms the basis of the fleet in the construction and agricultural sectors.

The leader in resales remains the ZiL 130, which indicates the continued demand for the cheapest vehicles for local tasks. Along with it, the GAZ and KamAZ models are in the top. At the same time, there is a gradual displacement of the outdated fleet by used European solutions, among which the greatest demand is for the Mercedes-Benz Sprinter (heavy versions), the T1/T2 series and Iveco Daily. Also, there is an active circulation of medium-tonnage Mercedes-Benz Atego and Renault Premium trunk vans, which indicates a slow but inevitable renewal of the fleet towards more reliable foreign brands.

Import of used equipment: Focus on logistics

Imports of used trucks from Europe are clearly focused on urban and regional logistics. The most popular body types are vans, in particular those equipped with tail lifts, as well as refrigerated trucks.

German manufacturers dominate the model ranking. The Mercedes-Benz Atego holds the lead, which is the de facto standard for distribution. It is strongly competed with by the MAN TGL, TGM and TGS truck line. It is important to note that mainly universal chassis are imported, which are easily adapted to the needs of a specific business. The top ten also includes heavy versions of the Volkswagen Crafter and specialized models such as the Mercedes-Benz Arocs or Axor, which emphasizes the marketʼs need for reliable equipment for difficult operating conditions.

New car and special equipment market

The new equipment sector (both imported and domestically produced) is focused on the municipal sector and highly specialized tasks. The priority types remain dump trucks, vans, and onboard platforms with cranes-manipulators.

The market leaders are Ukrainian enterprises that carry out construction on imported chassis. Models from UMP, SBM and InterCargoTruck form the basis of purchases for municipal needs (garbage trucks, road machinery). Among foreign brands, Iveco Daily, MAN TGS and Volvo FE hold stable positions. It is worth noting the presence of specialized lifting equipment from Zoomlion in the top, which reflects activity in the construction sector.

Conclusions

Analysis of the heavy truck market in February 2026 indicates a period of austerity and rationalization. A 60% drop in demand for new cars indicates the exhaustion of investment resources of large companies. The market is based on the internal circulation of old equipment and spot imports of used European trucks for logistics. Further dynamics will depend on the availability of credit programs for updating the outdated fleet, which currently consists mainly of equipment that has long exhausted its resource.

- Need more data? — contact IDA!