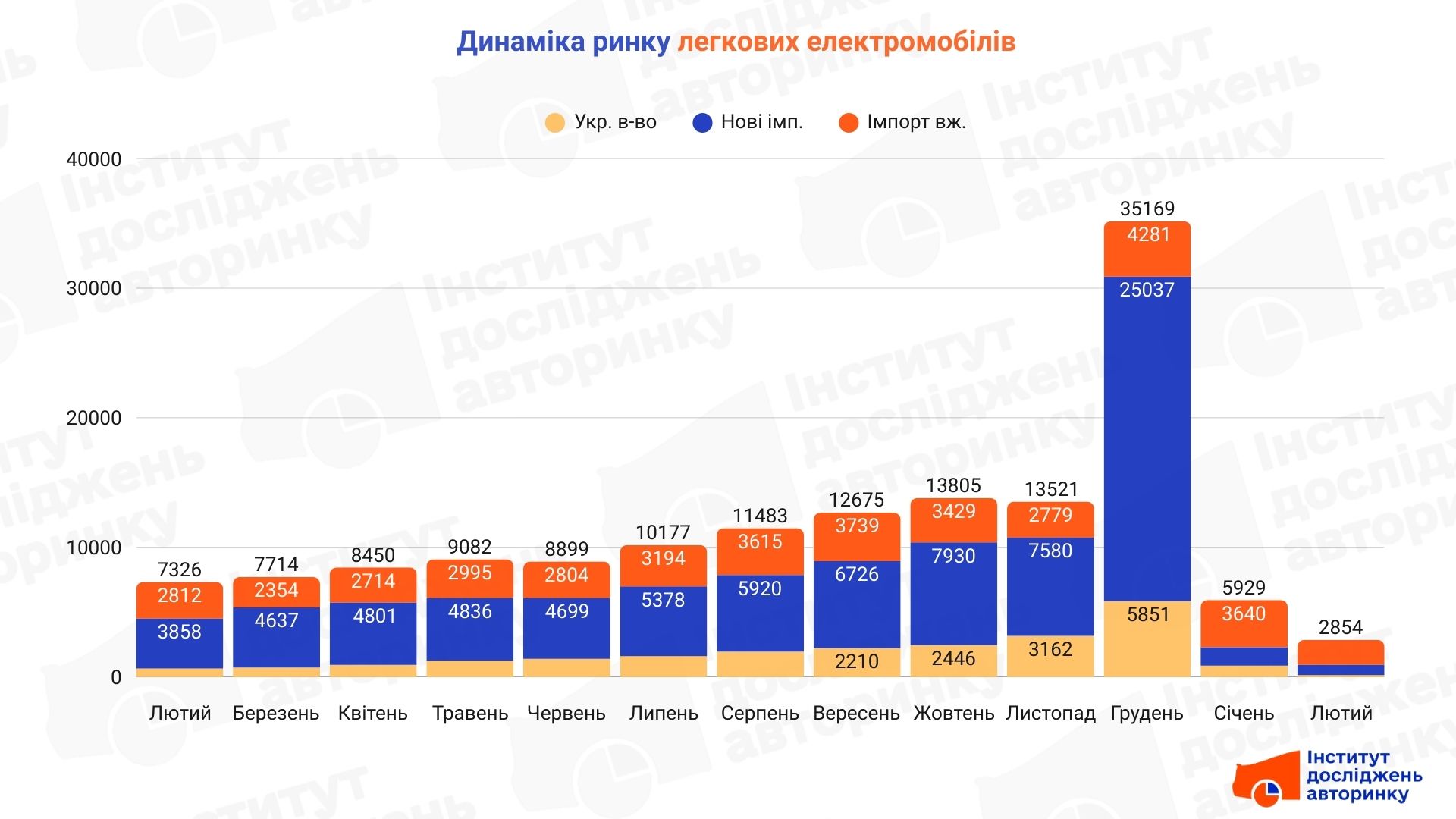

February 2026 was a period of deep correction in the electric car market. The main reason was the resumption of VAT on imports from January 1, which led to an anomalous peak in registrations in December 2025 and the subsequent exhaustion of "shifted" demand.

Statistical indicators:

- Domestic resales: 1,916 transactions. The figures fell by −47.4% MM and by −31.9% YY.

- Imports of used cars: 803 units. The segment showed a sharp decline: −43.2% MM and −79.2% YY.

- New: 135 units. The most vulnerable segment with a decline of −84.6% MM and −79.4% YY.

Market conditions have changed: the increase in the cost of imports due to the tax burden has forced buyers to either refocus on the domestic market or postpone purchases.

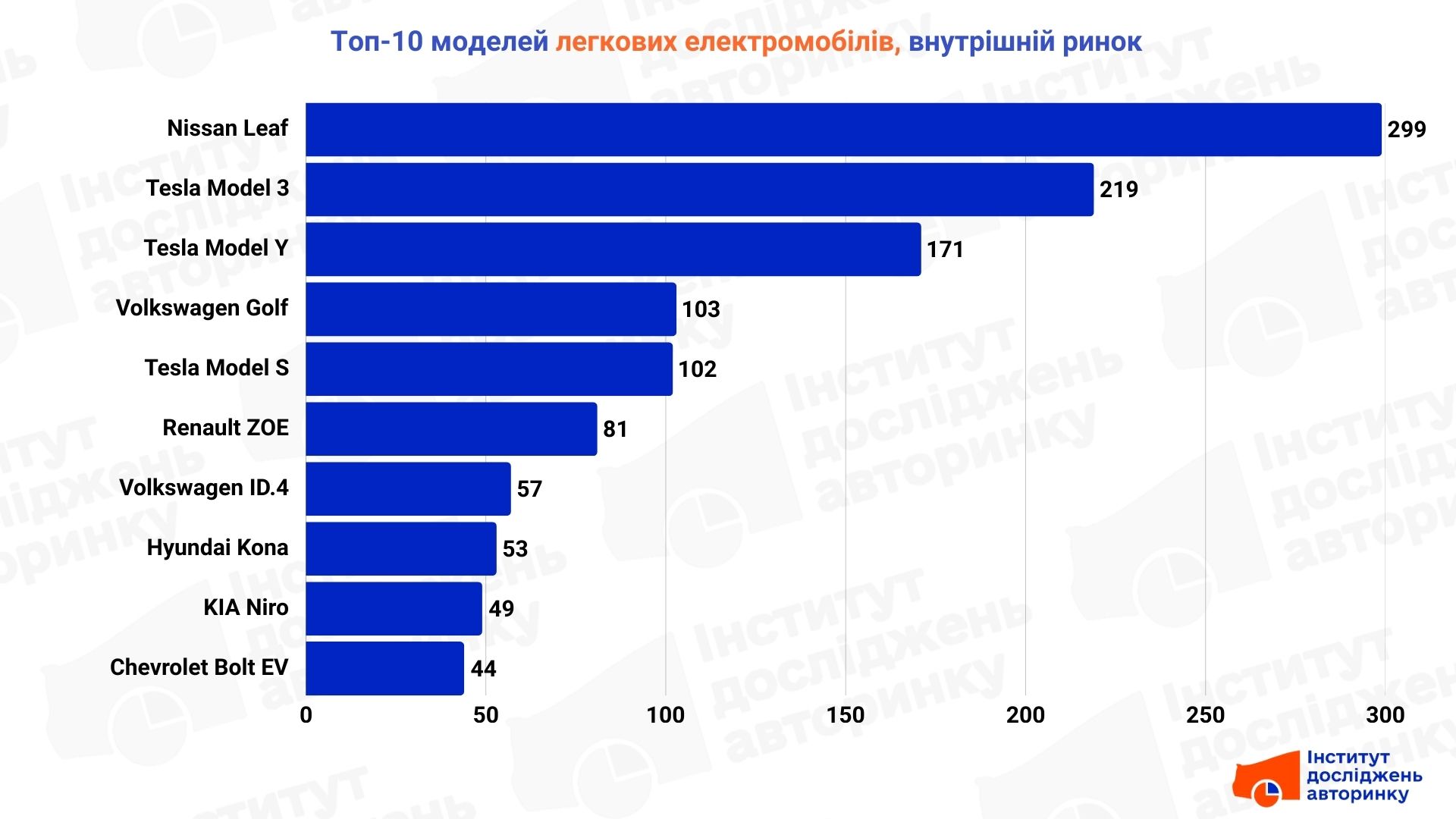

Top 10: Used cars (domestic market)

This segment remains the most stable due to the availability of vehicles in Ukraine and the lack of impact of new customs payments on already registered vehicles.

- Nissan Leaf: A solid choice for entering electromobility thanks to its simple design and affordability.

- Tesla Model 3, Model Y, Model S: Popular due to their developed service infrastructure and high technological level.

- Volkswagen e-Golf and Renault ZOE: Compact solutions valued for their European ergonomics and convenience in the city.

- Volkswagen ID.4: Gradually moving into the used category, remaining a favorite among crossovers.

- Hyundai Kona and KIA Niro: Chosen for battery reliability and balanced range.

- Chevrolet Bolt EV: In demand among those who need maximum range on a single charge in the budget segment.

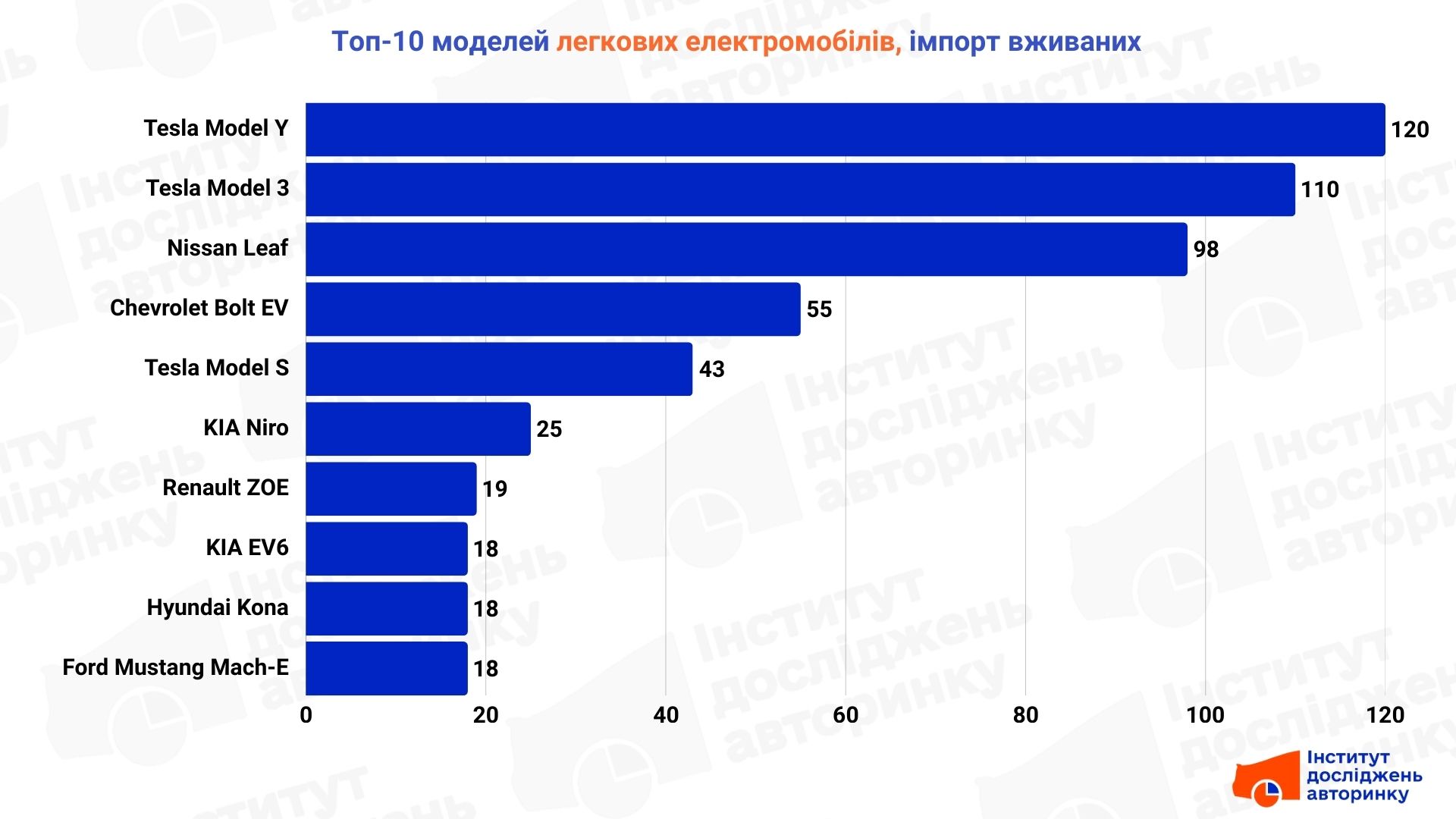

Top 10: "Prygon" of used cars

Despite the additional costs, imports from the US and Europe continue, but the focus has shifted to the most liquid models.

- Tesla Model Y and Model 3: The most sought-after pickup positions; they are valued for their ease of restoration and quick resale.

- Nissan Leaf: Continues to be imported as a proven budget solution.

- Chevrolet Bolt EV: Has a stable audience due to battery endurance.

- Tesla Model S: Remains relevant in the segment of comfortable used cars with a long range.

- KIA Niro and Hyundai Kona: Pragmatic imports from Europe and Korea.

- Renault ZOE: Often imported as a corporate vehicle or delivery vehicle.

- KIA EV6 and Ford Mustang Mach-E: Niche imports for those looking for individual style and modern architecture.

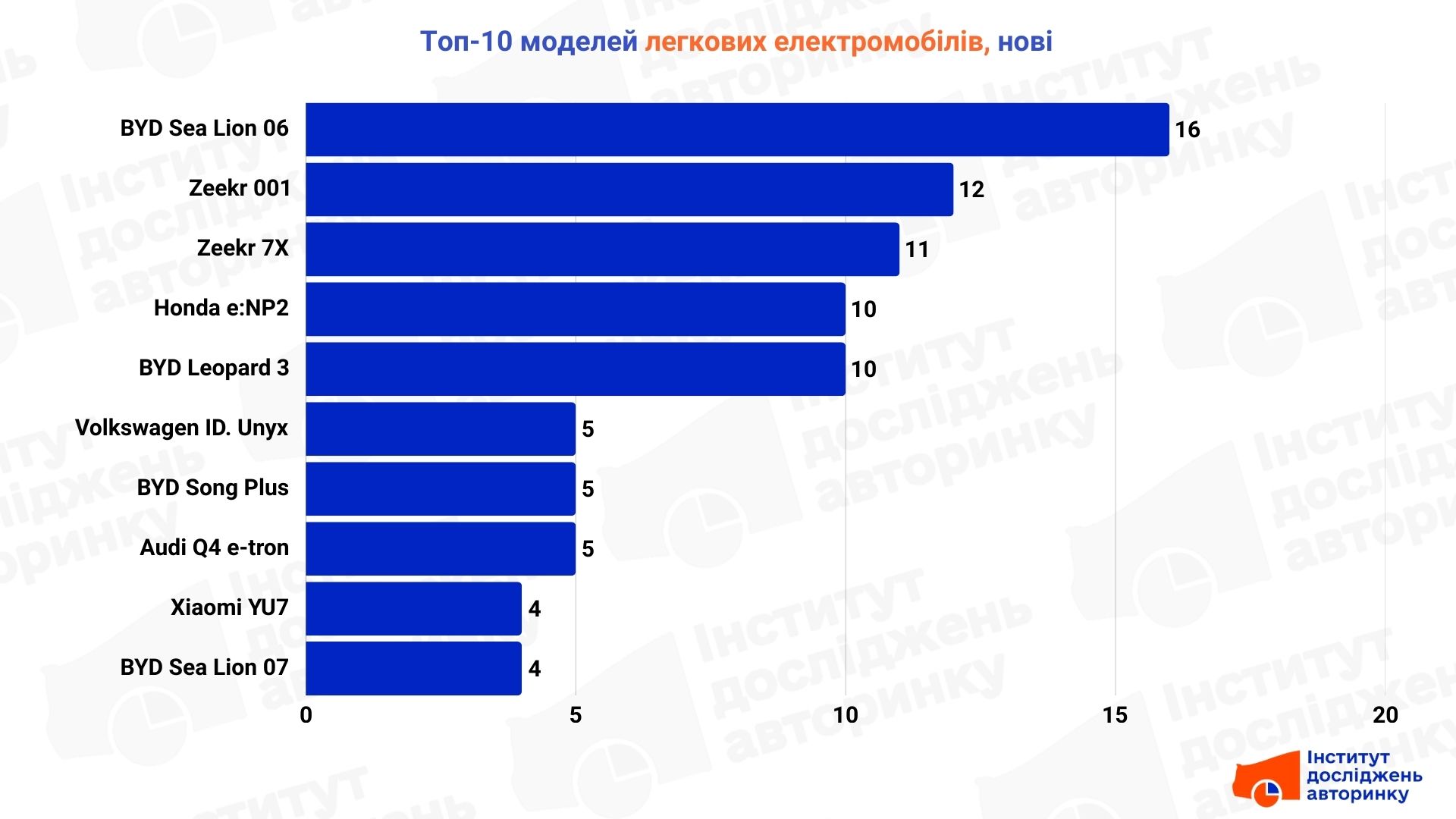

Top 10: New electric cars

The segment is completely occupied by Chinese brands and sub-brands (115 cars are produced in China, out of a total of 135), which offer the best price/technology ratio even including VAT.

- BYD (Sea Lion 06, Leopard 3, Song Plus, Sea Lion 07): The brand dominates thanks to its wide range of crossovers and its own innovative batteries.

- Zeekr (001 and 7X): Progressive premium, chosen for its dynamics and interior quality.

- Honda e:NP2: Chosen by conservative buyers for whom a familiar Japanese brand is important.

- Volkswagen ID. Unyx: A new vision of the ID line for those who want a familiar German brand in a new design, even if it is a Chinese product.

- Audi Q4 e-tron: the version from China, but still the one with the traditional four-ring emblem.

- Xiaomi YU7: The choice of an audience focused on gadgets and maximum integration of cars into the digital ecosystem.

The era of zero VAT is officially a thing of the past, and the February market (and ultimately, Januaryʼs) of electric vehicles met the new tax reality with a sharp decline. After the December hype, February 2026 demonstrated the expected but painful correction: imports of new cars collapsed by 84.6% MM, and the used car segment decreased by almost 80% year-on-year.

From which we can draw a number of conclusions, which are now visible much more clearly than they were in January.

- The significant decline in the domestic market indicates that the excitement at the end of 2025 was not related to attempts to speculate on VAT (to buy in 2025, and with the onset of 2026 to earn +20% due to changes in the rules). Because if this were the case, now we would see the growth of the "secondary". So, all last yearʼs cars were bought for personal use by 99%, if not 100%, and not as a "short-term investment for a rollover."

- China did “cover” the flow of new cars (the 180-day rule), which is evident from the statistics — despite the fact that among new ones there is a significant advantage in Chinese products, we, firstly, see very small volumes, and secondly — these may still be remnants from previous periods. The “Chinese” did not flow into the used category — there are only 34 such cars out of 803 that were first registered in our country.

- The VAT refund on the import of electric vehicles, which, although planned in the relatively distant 2021 as a temporary stimulus, did not have the expected effect of filling the budget with taxes. It simply “muffled” the import of electric vehicles to the level of 2021 — early 2022, when there were no additional car purchases. Here, citizens lost out, who, unlike a number of other countries, did not have “plus” state support (subsidies, grants, preferential loans, etc.) for the transition to electric transport, and now do not have support in the form of a tax discount. The state also lost out, which until now received a completely understandable benefit in the form of updating the fleet with environmentally friendly, safe and modern cars that are independent of fossil fuels. The linear calculation of virtual billions of “income” from an average of 7 thousand electric cars per month has turned into multiplying zero by high-profile ideas, as proven by recent statistics.

See more about the state of the electric vehicle segment in the video from the co-founders of the Institute for Automotive Market Research, Stanislav Buchatsky and Ostap Novytsky.

- Need more information or advice for your auto business — contact us!