Almost 40 thousand new and used cars made in China were purchased by Ukrainians during 2025. This is not just a successful year for Chinese brands — it is a real revolution. We are observing a phenomenon when “gray” or parallel imports have actually defeated traditional sales models, and hieroglyphs on the hood or display have ceased to scare buyers. This was discussed in a recent podcast by the head of the Institute for Car Market Research, Stanislav Buchatsky , and co-founder of IDA, Ostap Novytsky.

Ukraine in the context of Europe

The Ukrainian trend is part of a big game. In 2025, Chinese automakers sold about 811 thousand cars in Europe, which is almost twice (+99%) more than in 2024. The share of the "Chinese" in the EU market reached 6.1%. However, the structure of sales differs significantly.

In Europe, the MG brand (SAIC) is in the lead, having crossed the 300,000 car sales mark for the first time. In second place is BYD with a stunning jump of +276%. In Ukraine, the situation is unique: the top of the rating is occupied by models that were not intended for our market at all. This is a pure parallel import of cars manufactured for the domestic market of China. They are 30-40% cheaper than European counterparts, which became a decisive factor.

The Ukrainian market, on the other hand, has a unique specificity: there are almost no models in the TOP-15 that are officially supplied. These are "gray" imports of cars manufactured for the domestic market of China. They are significantly cheaper than European versions due to the lack of VAT on electric vehicles and aggressive pricing in the PRC.

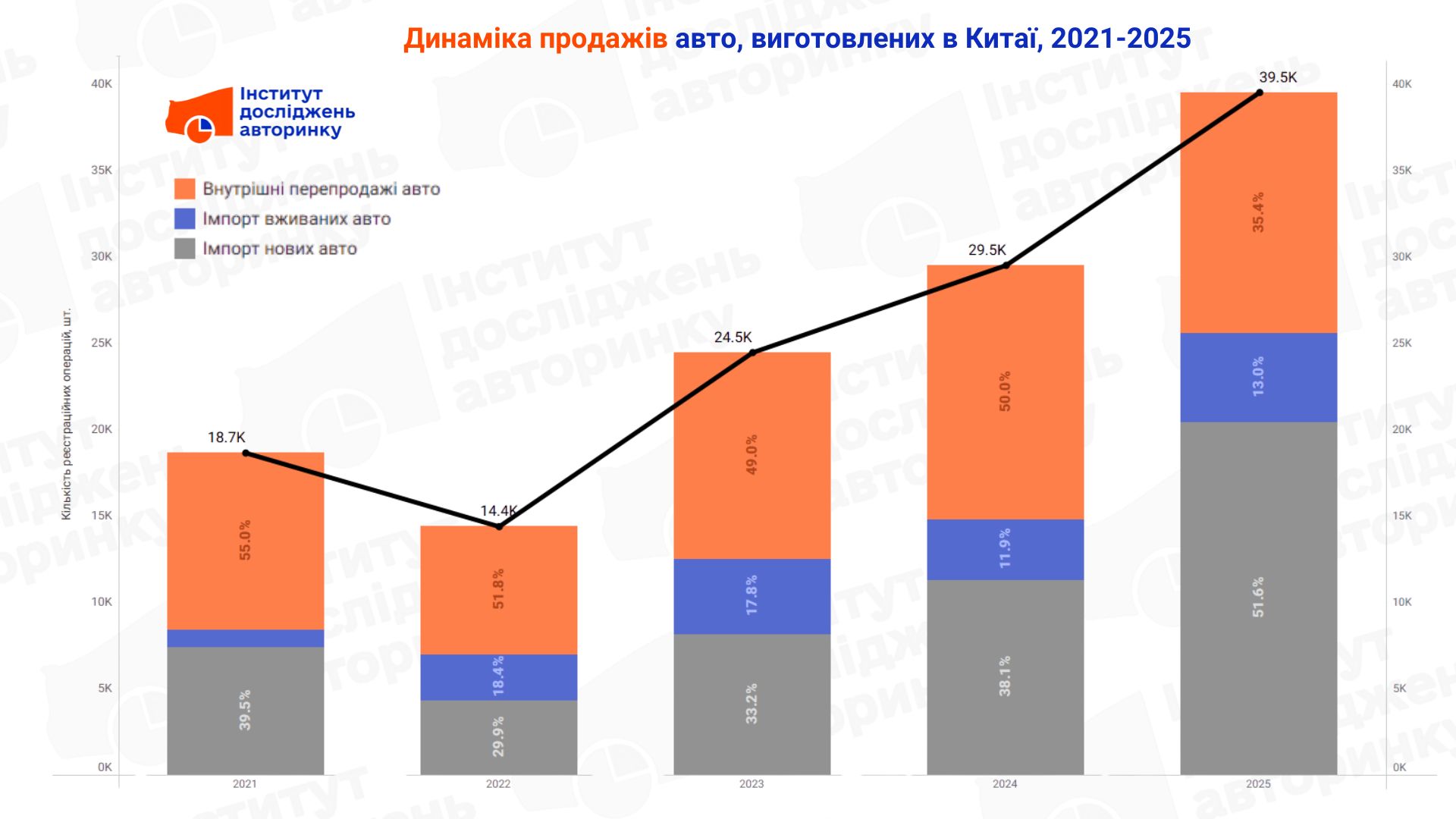

Chinese giants (FAW, SAIC, Dongfeng, GAC) have gone from copying Soviet and American trucks to creating joint ventures with Volkswagen, Audi, Honda and Mercedes. Having “pumped” Western technologies, China has added its own expertise in electronics and batteries. We can see the result in the sales dynamics diagrams.

Regional breakdown: Where do "gadgets on wheels" settle?

Analysis of registrations shows a clear relationship between infrastructure and demand. Almost 40% of all transactions are in the capital and Kyiv region ( 26.8% and 13.3%, respectively).

Next are large business hubs:

- Dnipropetrovsk region — 9.8%

- Odessa region — 8.7%

- Lviv region — 8.3%

This distribution is logical: large cities have the densest network of charging stations. In the conditions of a metropolis with its traffic jams, the savings factor becomes most noticeable for a resident who drives 50-80 km per day. At the same time, the periphery is still left out due to the low density of EV charging stations and possible power outages in rural areas. The economic factor, i.e. purchasing power, should not be ignored.

Why do we buy them?

The "Chinese" market in Ukraine is developing contrary to marketing rules. People buy cars without an official warranty, often without even seeing them in person — this is the "casino effect", where the risk is offset by incredible technological sophistication at a low price.

The main technical barrier is the GBT charging port. Chinese electric vehicles for the domestic market have their own port standard. In Ukraine, European CCS2 stations dominate. This creates a huge demand for new services: development of adapters and converters; software rework for Ukrainianization of interfaces; hardware rework of BMS boards for safe fast charging.

However, the market has crossed a critical threshold — 5% saturation. In economics, this is a “boom” point: when 5% of the population already uses a new type of product, it begins to be perceived as the norm.

In addition, the “gadget economy” factor is triggered. Chinese brands are updating their model range faster than buyers have time to get used to them. While a European manufacturer has been preparing a facelift for 4-5 years, the Chinese have been releasing three new models during this time. This creates excitement among buyers who want to own the most modern device, even if they had to wait three months for it to arrive from China.

What cars were bought from China? Top 15 models

The undisputed king of the market is BYD Song Plus (3,168 units). This is the flagship of the brandʼs "oceanic" series, which once started with batteries for mobile phones, and today independently produces everything from microcircuits to seat upholstery. Its success is based on the "Blade Battery" — a lithium-iron-phosphate battery that does not burn out even when physically pierced with a nail. This removes the main psychological barrier to electric cars, although from the point of view of driving the car remains purely family: the soft suspension is accompanied by a somewhat "cotton" steering wheel.

In the premium segment, the Zeekr brand, where Volvoʼs "Swedish blood" flows, caused a real sensation. The Zeekr 7X model (1,819 units) and the legendary shooting brake Zeekr 001 (1,663 units) became symbols of success in the IT environment. The design of the 001 model was developed in Gothenburg, and this is felt in the premium materials that significantly surpass the Spartan salons of the early Teslas. Here we see an 800-volt architecture and air suspension that changes the ground clearance, turning a sports car into a crossover. However, technical complexity has a downside: electric door drives can "live their own lives" after winter car washes, and the software requires professional flashing from hieroglyphs to understandable language.

A separate niche is occupied by “emotional” models, such as the BYD Leopard 3 (1,686 units) from the FangChengBao sub-brand. This is the choice of those who are tired of the usual design of European crossovers. The Leopard looks like a futuristic SUV with a backpack spare tire, offering an originality that conservative brands lack today. A similar story with the Denza N7 (471 units) is a former joint project with Mercedes-Benz. The Germans tuned the suspension and drew the design, and the Chinese gave their best electrical components and a Devialet audio system. This is a real “office on wheels”, where the level of comfort is close to the premium class of the German three.

The phenomenon of "Japanese" and "Germans" of Chinese origin is interesting. The Honda e:NS1 (1,310 units) and Honda e:NP2 (656 units) models are products of joint ventures with Dongfeng and GAC. This is the choice of conservatives: under the hood, the electric filling is arranged in such a way as to visually resemble a conventional internal combustion engine. This is "calming" engineering for those who are afraid of futurism. This also includes the Audi Q4 e-tron (1,189 units) and Volkswagen ID.4 (635 units). The latter, by the way, is rapidly losing ground. If two years ago the ID.4 was the undisputed leader, then in 2025 it will be ousted by newer models of the concern, such as the ID.Unix, due to outdated software and problems with "black screens".

The BYD brand continues to aggressively fill every price niche with its “marine” and “dynastic” lines. The Sea Lion 07 (1,422 units) demonstrates the pinnacle of integration: it uses a “12-in-1” module, where all electronics are collected in one block. Its “younger brothers” Sea Lion 06 (893 units) and Sea Lion 05 (579 units) offer rationality and minimal cost per kilometer. The budget segment is closed by the BYD Yuan Up (871 units) and the global hit BYD Yuan Plus (505 units), known in Europe as the Atto 3. This is the first Chinese model to receive 5 EuroNCAP safety stars, proving that Chinese engineering is no longer inferior to world standards.

Our ranking is closed by the only “official” one — MG ZS EV (400 units). This is a British brand with Chinese investments from SAIC Corporation. While other models in the top are purchased as a “casino ticket” without guarantees, MG offers official service. Although it does not have 40 screens or autopilot, the opportunity to come to a car dealership with a claim remains important for some Ukrainian buyers.

What next?

Concluding this analysis, it is important to raise a question that goes beyond the registration tables: what awaits these 40 thousand “gadgets” in 3–5 years? We have witnessed a unique moment when Ukraine has turned into a kind of “automobile sandbox” — a testing ground for Eastern technologies in conditions where there are no European protectionist tariffs, but there is a harsh climate and unpredictable energy.

The main challenge of the future is the secondary market. We are used to seeing an old Mercedes or Toyota valued for its engine life. In the case of Zeekr or BYD, we are entering the era of Software-Defined Vehicles (SDV). Here, the liquidity of a car will depend not on the condition of the suspension, but on whether updates come to it “over the air” and whether the central processor turns into a “brick” due to the cessation of support by the manufacturer. The used car market is facing a serious transformation: appraisers with thickness gauges will be replaced by cybersecurity and software diagnostics specialists.

This boom in Chinese cars also dictates new rules for business. We are no longer just importing hardware — we are importing ecosystems. If earlier “garage expertise” consisted of the ability to disassemble a chassis, then tomorrow’s leader in the service market is the one who is the first to crack the closed code of a Chinese cloud service to activate seat heating in Ternopil without requesting a server in Shenzhen.

And while Brussels and Washington are building tariff walls, Ukraine is showing the real picture: what a world looks like where the consumer has access to "pure" competition. We are a laboratory that European analysts are watching. It is possible that the way we now learn to service, reflash, and resell these machines will become a ready-made case for all of Eastern Europe in a few years.

Do you need detailed analysis of the Chinese car market in Ukraine or consultation? Our experts are waiting for your request!